Laxmi Organics Industries Ltd.

- Yash Mehta

- Mar 15, 2021

- 3 min read

Updated: Mar 25, 2021

IPO Details:

Price Band: 129-130

Cutoff Price: 130

About Company:

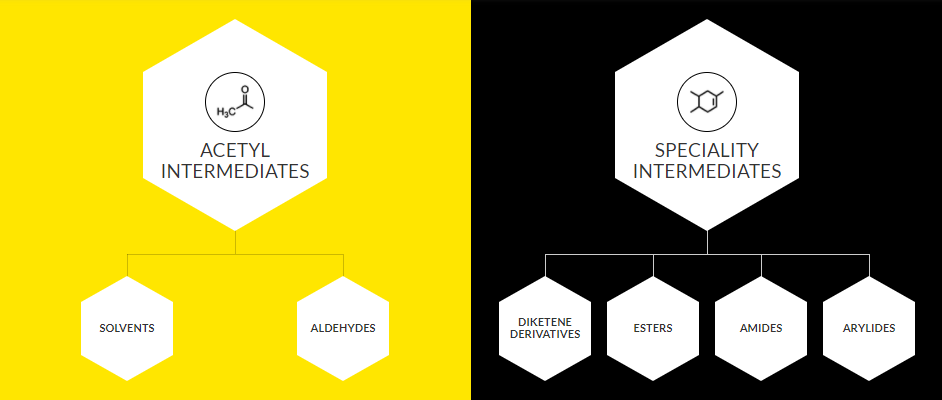

Leading manufacturer of Acetyl Intermediates and Specialty Intermediates with almost three decades of experience in large-scale manufacturing of chemicals. Since inception in 1989, Laxmi Organics have been on a journey of transformation. It initially started manufacturing acetaldehyde and acetic acid in 1992, and soon thereafter moved on to manufacturing of ethyl acetate in 1996. They are currently among the largest manufacturers of ethyl acetate in India with a market share of approximately 30% of the Indian ethyl acetate market. Further, post completion of the YCPL Acquisition, their market share in the ethyl acetate market will be further enhanced. In Fiscal 2010, the company began manufacturing the Specialty Intermediates by acquiring Clariant’s diketene business. Company believe that the diversification of their product portfolio into varied chemistries in Specialty Intermediates has enabled them to create a niche for themselves.

Laxmi Organics is the only manufacturer of diketene derivatives in India with a market share of approximately 55% of the Indian diketene derivatives market in terms of revenue in Fiscal 2020 and one of the largest portfolios of diketene products.

Competitive Strengths:

Leading manufacturer of ethyl acetate with significant market share

Only Indian manufacturer of diketene derivatives with a significant market share and one of the largest portfolios of diketene products

Diversified customer base across high-growth industries and long-standing relationships with marquee customers

Strategically located manufacturing facilities, vertical integration and supply chain efficiencies

In-house research and development capabilities and consistent track record of technology absorption

Global presence and low geographical concentration

Differentiated business model, asset base, product mix and experience in handling complex chemistries create high entry barriers

Experienced promoter, board of directors and key managerial personnel

Strategies:

Volume maximisation at Manufacturing Facilities by expanding installed capacities to support growth initiatives

Expanding and optimising product portfolio

Increasing the global footprint and augmenting growth in current geographies;

Establishing fluorospecialty chemicals business

Continuing focus on innovation and leveraging chemistries and technology absorption

Impact of the COVID-19 pandemic on our business operations

Financial Performance:

Blue Bar is Revenue, Red Bar is Net Profit, Yellow Bar is EPS

Company's EPS is decreasing for last three years and revenue is more or less stable.

Objects of the Issue:

The Offer comprises the Offer for Sale and the Fresh Issue.

Offer for Sale: The proceeds of the Offer for Sale shall be received by the Promoter Selling Shareholder. Company will not receive any proceeds from the Offer for Sale.

Fresh Issue:

Company proposes to utilise the net proceeds of the Fresh Issue, i.e. gross proceeds of the Fresh Issue less the Offer related expenses applicable to the Fresh Issue and the proceeds from the Pre-IPO Placement towards funding the following objects:

Investment in wholly owned Subsidiary, Yellowstone Fine Chemicals Private Limited for part-financing its capital expenditure requirements in relation to the setting up of a manufacturing facility for fluorospecialty chemicals

Investment in YFCPL for funding its working capital requirements

Funding capital expenditure requirements for expansion of SI Manufacturing Facility

Funding working capital requirements of Company

Purchase of plant and machinery for augmenting infrastructure development at SI Manufacturing Facility

Prepayment or repayment of all or a portion of certain outstanding borrowings availed by Company and wholly owned Subsidiary, Viva Lifesciences Private Limited.

Our view: With EPS of Rs 2.86, company cutoff price is valued at P/E of 45 and price to net worth is 6.9. Objective of the issue is OFS and also using capital for the operation which is positive about the IPO. It possess Grey Market Premium (GMP) of around 88% which is good for listing gains. I would apply for this IPO only for listing gains as of now.

Do visit this blog and the link after 6pm to get updated details on grey market premium and subscription details.

Grey Market Premium:

Subscription Details:

Allotment Status: Link

Listing Status:

Disclaimer: Views are shared for educational purpose. Please consult your financial advisor or planner before taking any action based on the views or facts shared on this blog.

I hope you all will like the summary of the Laxmi Organics IPO. Please like and share with others too so that they can gist of this IPO.

Thanks You all for giving your precious time to read this blog.

Comments